Compare fixed rate mortgages

Fixed Rates

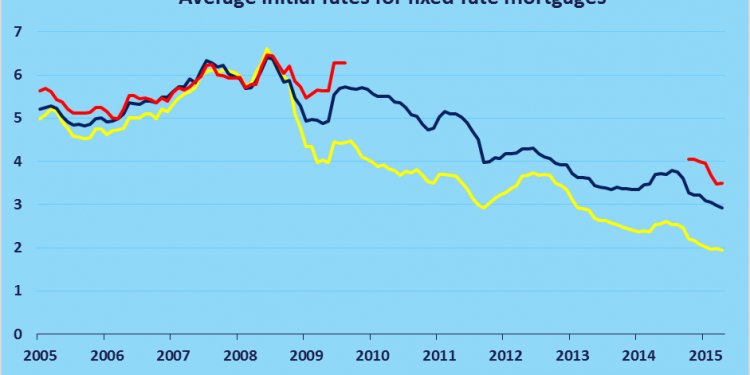

Fixed-rate mortgages are the most common way to finance a home in the United States. They allow home buyers to lock in a set APR and stable monthly payment for the duration of the loan.The most popular term is the 30-year mortgage, but the 15-year option is not uncommon.

The primary benefits of FRMs are

- helps buyers build equity in their home;

The drawbacks of FRMs are

- higher initial monthly payments;

- higher initial APR - though they are lower than the maximum ARM cap rates & can be refinanced if rates drop

Adjustable Rates

Do you know what they call an adjustable-rate mortgage in Europe?

A mortgage.

That's because homebuyers in most of the civilized world have only one option when financing a house, the ARM, often called a variable rate mortgage outside the United States.

In the US, we can choose between an ARM and a FRM, and because the latter offers the security of an unchanging APR with no surprises, it's more popular.

However, there are hundreds of thousands of Americans who have benefited from taking out ARMs, so it just might be a good fit for your lifestyle and your future.

What is an ARM?

An ARM is a mortgage with an initial interest rate that lasts for a few years and then adjusts once a year after that. We're not going to sugarcoat it for you - your interest rate (and monthly mortgage payment) will most likely go up after the ARM's introductory period. By how much? That depends on the real estate market a few years from now, as well as the economy in general.

Fortunately for consumers, ARM rates come with a ceiling or cap, ensuring that your rate won't spiral out of control at the end of the initial rate period. However, there are some exceptions to the rate cap guaranteed by an ARM agreement.

An ARM is more of a calculated risk than a gamble, but it can be very rewarding in the long run - or we should say - in the short run. This something we'll have to explain later, though.

All ARMs are based on a 30-year loan term, and that's one of the few constants in this type of home financing. The length of the initial rate, the interest rate afterward, and the value of your home are all subject to change.

The Most Common Reset Points

Let's call the initial period during which time your introductory rate is preset the “honeymoon period.” The average one lasts about 5 years, but you can hammer out any deal you want, so long as the total loan period works out to exactly 30 years.

After the honeymoon period, your interest rate and monthly payment adjusts to the going rate. This is called the reset point, and it can play a big part in your ARM's success.

Share this article

FAQ

How to get the best refinance rate on my mortgage without having hard inquiries on my credit report - Quora

If you only focus on getting the "lowest rate" you may be charged higher fees. It's like playing chess. If you only look at some pieces on a chess board, your opponent will take your queen or rook while you're not paying attention.

Related Posts

Latest Posts