Local interest rates

Twitter LinkedIn Google Plus

Twitter LinkedIn Google Plus

Terry examines the multiple factors behind the lackluster stock market performance in regions with negative interest rate policies.

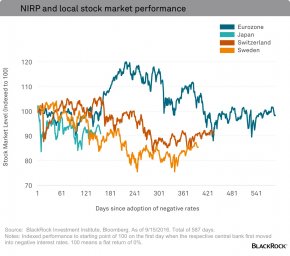

Stock market performance in regions with negative interest rate policies has been underwhelming. It’s true that global investors have enjoyed a seven-year bull market in big part due to unprecedented monetary policy accommodation. But has negative interest rate policy (NIRP) been an additional catalyst? Based on the local stock market returns alone, the answer is no.

Some background first. There are currently five regions globally with negative interest rate policies—the eurozone, Japan, Switzerland, Sweden and Denmark—versus none five years ago. The aim of NIRP, like the aim of more conventional zero interest rate policy (ZIRP), is to push investors away from safe assets (e.g., government bonds) to riskier assets (e.g., stocks and fixed income credit). But the results have been somewhat questionable.

Looking at the chart below, the eurozone was the only local market to see positive performance after the introduction of negative rates, but that didn’t last. However, we think there are multiple factors behind the lackluster stock market performance in these regions, and it’s important to consider them before making a judgement on the effectiveness of NIRP.

Figuring out the equation

Drilling down into the basic valuation equation (shown below) helps illuminate a couple of these factors. What is the price of a stock or stock market? A stock market price is the present value of companies’ future earnings divided by the discount rate, usually referring to a short-term Treasury yield, plus an equity risk premium (ERP). In other words, it’s the price investors are willing to pay today, assuming the price will grow at the discount rate to match the companies’ expected future earnings.

If the discount rate is reduced to 0% or below (i.e. based on a government’s short-term rate) and the ERP stays constant, the price of a stock market should rise. This is essentially what happened immediately after the financial crisis when developed market central banks acted very aggressively with ZIRP.

Why isn’t this happening now for local stocks? Let’s look at the two remaining variables in the basic valuation equation.

The ERP can be thought of as the compensation for an investor placing cash into equities in contrast to maintaining it in some risk-free asset (e.g., a U.S. Treasury bill). If you look at the basic valuation equation again (see the modified version below), a declining ERP (shown with a green down arrow) should increase the value of a stock market, with all other parts of the equation being equal. Conversely, an increasing ERP, represented by a red up arrow below, should lower the price of the market. Recently, the eurozone ERP has slightly increased as interest rates have declined, and the Japanese ERP has been flat since end of 2015.

Also driving the valuation of a stock market is future earnings (i.e., earnings projections). If future earnings are declining (see red down arrow below) at a faster rate than central banks are cutting interest rates, then the price of a stock market will continue to decrease as analysts become less optimistic. This is what we are seeing in Europe and Japan (as well as in other regions). A double-dip recession and the unknown impact of Brexit in the eurozone, and on-and-off recessions in Japan, have been deterrents to higher earnings projections in those markets.

In fact, macroeconomic data tend to have a larger influence on stock market prices over the long run than interest rates, as empirical evidence shows. If all that mattered to stock market performance was the level of interest rates (at zero or below), then rising stock markets would be a persistent phenomenon. Weaker-than-expected economic data tend to lead to reduced earnings estimates and projections, and in turn, lower stock market prices, for example in the eurozone and Japan.

What’s the answer?

Monetary policy has been a key driver of asset prices in recent years, but its effectiveness looks to be waning (see our midyear outlook). We believe catalysts for upside stock market movement in NIRP regions will need to come from economic and earnings growth.

Terry Simpson BlackRock Investment Institute. He is a regular contributor to The Blog.

Investing involves risk, including possible loss of principal. International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation and the possibility of substantial volatility due to adverse political, economic or other developments. These risks often are heightened for investments in emerging/ developing markets, in concentrations of single countries or smaller capital markets.

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of September 2016 and may change as subsequent conditions vary. The information and opinions contained in this post are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This post may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this post is at the sole discretion of the reader.

©2016 BlackRock, Inc. All rights reserved. BLACKROCK is a registered trademark of BlackRock, Inc., or its subsidiaries. All other marks are the property of their respective owners.

Share this article

FAQ

How to get the best mortgage rates - Quora

I agree with Michael Cheng. If you have a great credit score, stable, verifiable income, verifiable cash on hand or assets, you are a dream client. By comparison shopping, you will be able to obtain a Loan Estimate from at least three different types of lenders: Talk with the mortgage department of where you currently bank. You already have a banking relationship with them. This is a good place to start. Next, apply with a local, licensed non-bank mortgage lender. Somebody located in the town in which you live. Last, apply with a local mortgage broker.

Related Posts

Latest Posts