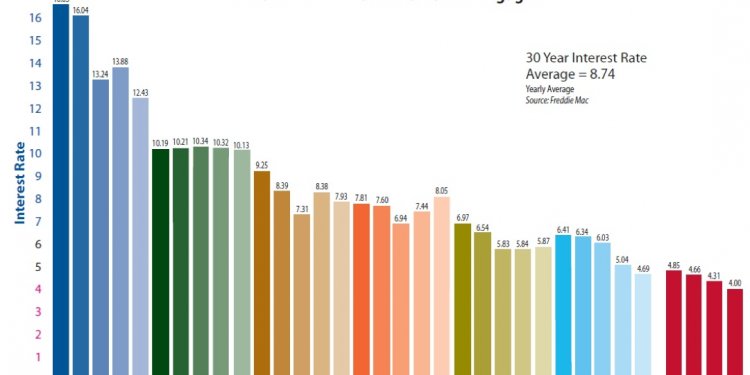

Conventional Mortgage Rates

Buying a home is perhaps the largest investment you’ll make in your lifetime, so it’s important to choose the right mortgage from the start. You have several types of loans to choose from, including a conventional mortgage, and each has a different set of requirements.

Buying a home is perhaps the largest investment you’ll make in your lifetime, so it’s important to choose the right mortgage from the start. You have several types of loans to choose from, including a conventional mortgage, and each has a different set of requirements.

A conventional mortgage is a home loan that isn’t guaranteed or insured by the federal government and conforms to the loan limits set forth by Freddie Mac and Fannie Mae. You can get a conventional loan at a fixed or adjustable rate.

Three other options — FHA, VA and USDA loans — are backed by the federal government. Loans guaranteed by the Federal Housing Administration aim to make buying homes more affordable for low- to middle-income families by offering low down payments. VA loans are guaranteed by the U.S Department of Veterans Affairs and are available to active military and veterans only. Finally, USDA loans are backed by the U.S. Department of Agriculture and are geared toward buyers of rural properties.

GET EXPERT ANSWERS TO YOUR MORTGAGE QUESTIONS

Get personalized help from an unbiased mortgage broker. Understand your options and find the best rates.

COMPARE MORTGAGE RATES FOR FREE

See personalized mortgage rates in seconds using our comprehensive mortgage tool.

Conventional loans, on the other hand, are offered by private entities such as banks, credit unions, private lenders or savings institutions. Because they are not guaranteed by the government if the buyer defaults, they’re a higher risk for lenders.

Conventional loans also require a larger down payment, so those buyers tend to have a more secure financial standing and are less likely to default. The larger down payment also means lower monthly payments. Plus, with the ever-increasing mortgage insurance premiums on FHA loans, payments for conventional loans can be much more manageable in comparison.

Conventional mortgage Basics

Conventional mortgage Basics

The term (or length) of a conventional loan is usually 15, 20 or 30 years. These mortgages are available to everyone, but borrowers need good credit to qualify. Requirements vary from lender to lender, but 620 is typically the minimum credit score needed to obtain a conventional loan, and 740 is the minimum score you need to get a good rate.

A conventional mortgage also requires a sizable down payment in comparison to other types of mortgage loans. Borrowers can put down as little as 5%, but conventional lenders typically require up to 20% for a down payment; the amount can vary based on the lender as well as the borrower’s credit history.

In addition to the down payment, borrowers are often responsible for origination fees, mortgage insurance and appraisal fees. As such, conventional loans tend to have a higher out-of-pocket cost at closing than other types of mortgage loans.

Loan limits

Conventional mortgages fall into two categories: “conforming” and “non-conforming” loans.

Conforming loans follow the guidelines set by Fannie Mae and Freddie Mac, two government-controlled companies that provide money for the U.S. housing market. The most well-known rule has to do with the size of the loan. In 2016, home loans for single-family homes in most of the continental U.S. are limited to $417, 000. Higher-cost areas, such as Hawaii and Alaska, have higher limits up to $625, 500 for single-family homes.

Non-conforming loans, often called jumbo loans, are for borrowers who don’t qualify for a conforming loan because the amount is higher than the conforming limit for the area. Because they don’t conform to the guidelines, jumbo loans are usually harder to sell on the secondary market (when lenders sell their loans to other institutions), making them less attractive to lenders. And the higher amount of money involved also means more risk for the lender.

Other types of non-conforming loans include those made to borrowers with poor credit, high debt or recent bankruptcy, or on homes with a high loan-to-value ratio (usually up to 90% for a conforming loan).

Lenders typically charge higher rates for non-conforming loans, and they may carry other fees or insurance requirements due to their riskier nature.

Conventional loans are an excellent option for borrowers with strong credit who can contribute a down payment of at least 5%, or perhaps quite a bit more. Compare the benefits of a conventional mortgage with those of FHA and VA loans to determine which product best suits your needs.

Share this article

Related Posts

Latest Posts