New Housing Loan Programs

Effective December 1, 2016 the new annual premium of 0.25 percent of the remaining loan balance will apply to all new loan guarantees, including refinances. Read the full Federal Register Notice HERE. Frequently Asked Questions HERE.

Program Overview

The Section 184 Indian Home Loan Guarantee Program is a home mortgage product specifically designed for American Indian and Alaska Native families, Alaska villages, tribes, or tribally designated housing entities. Congress established this program in 1992 to facilitate homeownership and increase access to capital in Native American Communities.

Section 184 is synonymous with home ownership in Indian Country.

|

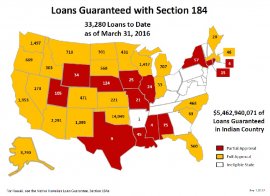

As of March 31, 2016, the Section 184 program has guaranteed over 33, 000 loans, representing over $5.4 billion dollars in increased capital into Native American Communities. |

How Section 184 Works

The Office of Loan Guarantee within HUD’s Office of Native American Programs, guarantees the Section 184 home mortgage loans made to Native borrowers. The loan guarantee assures the lender that its investment will be repaid in full in the event of foreclosure.

The borrower applies for the Section 184 loan with a participating lender, and works with the tribe and Bureau of Indian Affairs if leasing tribal land. The lender then evaluates the necessary loan documentation and submits the loan for approval to HUD’s Office of Loan Guarantee.

The loan in limited to single-family housing (1-4 units), and fixed-rate loans for 30 years of less. Neither adjustable rate mortgages (ARMs) nor commercial buildings are eligible for Section 184 loans. Maximum loan limits vary by county. Click on the link below for the most current loan limits.

By encouraging lenders to serve Native communities, Section 184 is increasing the marketability and value of the Native assets and strengthening the financial standing of Native communities.

Eligible Borrowers

- American Indians or Alaska Natives who are members of a federally recognized tribe

- Tribally designated housing entities

- Indian Housing Authorities

Eligible Areas

Loans must be made in an eligible area. The program has grown to include eligible areas beyond tribal trust land. Click on the links below to determined participating States and counties across the country.

Share this article

FAQ

What happens when the Federal Reserve buys mortgage-backed securities? - Quora

How difficult is it to buy mortgage backed securities?

Related Posts

Latest Posts